What’s next for the rent review?

As we approached summer in 2025, the Government proposed a major reform affecting business tenancies under the current version of the English Devolution and Community Empowerment Bill, that upward only rent review (UORR) provisions will be prohibited in new commercial leases.

The proposed changes will not retrospectively affect leases already granted, but it would apply to lease renewals and new leases.

The provisions came without industry consultation, which has drawn attention and much criticism from the sector. Organisations have been engaging with Parliament on this following its unexpected inclusion in the Bill.

It is suggested that the proposal stems from a declining high street and retail town centres, of course outside of residential, being the media darling protected sectors.

An UORR is where the rent review mechanism will generally state, ‘the rent will be reviewed to the higher of the passing rent or the market rent’ which in essence means that it cannot go down but it can stay the same or it can increase.

The government maintains that upwards only rent reviews are a contributing factor in the decline of town centre retail, as they can lead to artificially inflated rents which unfairly penalise tenants, and in turn leading to vacant premises. It seems like a broad-brush approach and a desperate bid to wave a magic wand. Surely business rates, free car parking and business enterprise grants are more instrumental in the vitality of town centres and the UK high street.

The ban will apply to any rent review mechanism where, at the date of grant of the lease, the rent to be paid following a review is uncertain or cannot be determined, thus we could potentially see an end to:

- Upwards only open market rent reviews;

- Index linked rent reviews with a collar or floor i.e. that ensure a minimum uplift in rent; and

- Leases where rent is linked to turnover where a minimum base rent is reserved.

So, what are the potential market implications?

- Leases become shorter – it will be easier to propose lease terms of 3 to 5 years with no rent review whatsoever. This can impact landlord security of income for medium to long term and would affect investors in terms of investment value.

- Impact on negotiations – even before it is law, upward/downward review may become a negotiation point on many lease transactions. Will tenants look for extended incentives (such as rent free, or capital contribution to fit-out) if landlords are seeking higher starting rents?

- The possibility of downward review may lead to fewer disputes and tenant financial problems in depressed markets.

- Investment strategy may put a higher premium on long-term occupation by strong covenant occupiers.

- Landlords with shorter term occupiers will need to be proactive – unless the passing rent is below market rent and therefore reversionary on renewal. Otherwise, if rent passing is rack rented, it may force a landlord to offer incentives to occupiers on renewal (if wanting to maintain passing rack rent), or undertake improvement works to the property to induce occupiers to renew.

- Debt arrangements – there will be issues for certain finance structures if upwards only rent reviews were used as an assumption to obtain rental growth throughout a lease term and life cycle of an investment holding.

- Reduction in forward funding on speculative developments – investors like to see guaranteed returns at a minimum level which can service debt (if applicable) and to provide a sufficient rate of return on an investment, by having upward only reviews or an index linked cap and collar review mechanism. Without this at the outset, it is difficult to forge return forecasts into an appraisal if you only have open market (can go downwards) reviews. The option to alleviate risk is to include fixed rental increases throughout the term or to have index linked reviews but set at an actual level without the ‘jeopardy’ of cap and collar.

The most immediate consequence will be landlords offering shorter lease commitments. Upward only rent reviews have historically enabled landlords to offer longer term leases with confidence that rental income would keep pace with inflation and market conditions.

There is understandable concern within the property industry that these proposals could lead to uncertainty around commercial property.

The Bill in its current form could lead to a substantial revaluation of investment properties and a stifling of the market. Even in the absence of such extreme impacts what we could end up seeing is shorter lease terms to enable rents to be rebased more frequently or leases with fixed rental increases, pure index-linked rents or formula-based stepped rents. Whether it will lead to a return to the bustling high streets that the government are aiming for remains to be seen.

What should landlords do now?

It is prudent to start adapting to what is likely to become law as that becomes more certain through the process.

Landlords should:

- Consider at a strategic level how a ban on upwards only rent review would impact modelling and valuation within the business. Some analysts may consider modelling potential income drops at future review points – but remember that the prohibition does not apply to existing leases – so this sort of modelling should only be done to hypothetical future income projections.

- Ensure agents and asset managers on the front line of negotiation of new leases are briefed to expect an increase in requests for upward/downward rent review – and take a short-term position on the point pending progress of the new law.

- Monitor the Parliamentary progress and engage with industry bodies.

We asked Ian Liddle, Commercial Property partner at Farleys Solicitors LLP, now part of the Lawfront Group, for his expert opinion with the following questions:

Q. As the proposal seems to be a sticking plaster to the high street and retail in town centres, could you see that the Bill becomes diluted to specifically apply to only retail leases, or will this be across all commercial sectors?

A. The current drafting applies across all business tenancies, not just retail or high street. It covers:

- All tenancies under Part II of the Landlord & Tenant Act 1954, including both contracted-out and in-standard leases.

- Office, retail, logistics, industrial, licensed premises, etc.—basically any business lease where rent review clauses like open-market, index-linked, or turnover-based are used.

- Stepped/fixed rents remain outside the ban.

While the policy was motivated by high‑street concerns, no carve-out exists for retail-only. Any sector using those mechanisms is impacted.

Q. Are there ways around this? For example, deliberately not triggering a rent review as a Landlord?

A. Landlords will need to adapt but direct “avoidance” is limited by anti-avoidance clauses and restrictions:

- Permitted structures include:

-

- Fixed or stepped increases (e.g., 3% annual uplifts).

- Index-linked reviews (CPI/RPI), so long as they allow for downward movement.

- Turnover-based reviews, again as long as with potential for rental reduction.

- Caps and collars may be introduced through secondary legislation —though collars set below the starting rent could be prohibited to prevent circumvention.

- Anti-avoidance measures will render void:

- Side letters/agreements that top-up downward reviewed rents

- Put options and other mechanisms meant to preserve upward-only outcomes.

- Delaying a review: the Bill empowers tenants to trigger or force rent reviews if landlords delay them, preventing landlords from postponing a rent review in a falling market.

So, rather than looking at ways around, I suspect that the market will shift towards alternative structures (fixed uplifts, indexation, turnover) rather than hinge on avoidance.

Q. What happens to the role of the ‘Third Party’ surveyor as Expert Witness or Arbitrator. This will surely become less required if there are less open market reviews being implemented or triggered?

A. The ban on upward-only reviews may reduce open-market rent reviews, but this doesn’t completely eliminate the need for expert determination:

- Index-linked increases and fixed uplifts generally don’t require expert valuation, so fewer triggers for surveyor-led market assessments.

- However, disagreements over interpretation of clauses, the level of caps/collars, or index application could still lead to arbitration or expert determination.

- The role of third-party surveyors as arbitrators or “expert witnesses” remains relevant in:

- Disputes over market rent resets (where open-market still occurs but bidirectional),

- Determining ambiguous lease terms,

- Reviewing turnover or index application,

- Reviewing upward only rent review clauses in leases which were completed before the implementation of the ban.

In summary, while the volume of open-market reviews may decline, the need for objective third-party oversight will continue, especially in contested outcomes.

Q. What happens next?

A. Key next steps through Parliament and beyond:

- Parliamentary timetable:

- Currently undergoing Committee Stage in the House of Lords (Jan–Feb 2026).

- Followed by Report Stage, Third Reading, then Royal Assent, likely in mid-2026.

- Post‑Royal Assent:

- Secondary legislation will define commencement dates, implementation timelines, and any caps/collars exemptions.

- Expect consultation on details such as regulatory boundaries for index-linked reviews.

- Market preparation:

- Law firms, landlords, and occupiers are already analysing drafting strategies.

- During 2026, we’re likely to see guidance and lease precedent shifts.

- The effective implementation date is expected between 2027–2028, though that could be adjusted based on secondary regulations.

It appears that there is still some way to go to until we get more transparency on what will be incoming, and Wildbrook, and Farleys, will be on hand to guide investor clients accordingly through the process.

Thanks to Ian Liddle.

Ian is a Joint Managing Partner at Farleys. He is a highly respected commercial lawyer with over 35 years’ experience, which he brings to his role in guiding the strategic direction of Farleys, and continuing to build the firm’s presence and reputation as one of the region’s leading law firms.

Regularly featured for his work in the Legal 500, Ian continues to head up and be heavily involved in the work of Farleys’ commercial team, which he established over 20 years ago. With expertise in commercial property, corporate insolvency, and contract matters, his clients appreciate his pragmatic approach and his ability to provide clear and concise legal advice.

Contact: [email protected]

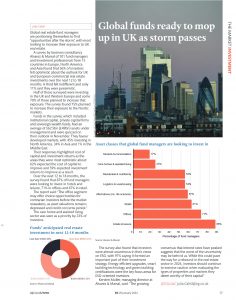

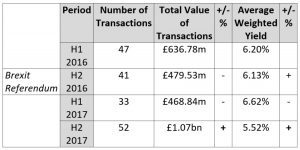

Those sitting on their hands (buyers and sellers), I wonder what will happen post October 31st Brexit deadline. Will the market fall off a cliff? – highly unlikely. Will anything happen by 31st October? – unlikely, given current political situation. So, if a decision could be made now to buy or sell an asset, then October should not be a decisive factor. We always say that if a deal is good on paper, and the real estate fundamentals are good i.e. good location for sector and quality real estate to re-let if required, then why sit on your hands?

Those sitting on their hands (buyers and sellers), I wonder what will happen post October 31st Brexit deadline. Will the market fall off a cliff? – highly unlikely. Will anything happen by 31st October? – unlikely, given current political situation. So, if a decision could be made now to buy or sell an asset, then October should not be a decisive factor. We always say that if a deal is good on paper, and the real estate fundamentals are good i.e. good location for sector and quality real estate to re-let if required, then why sit on your hands?